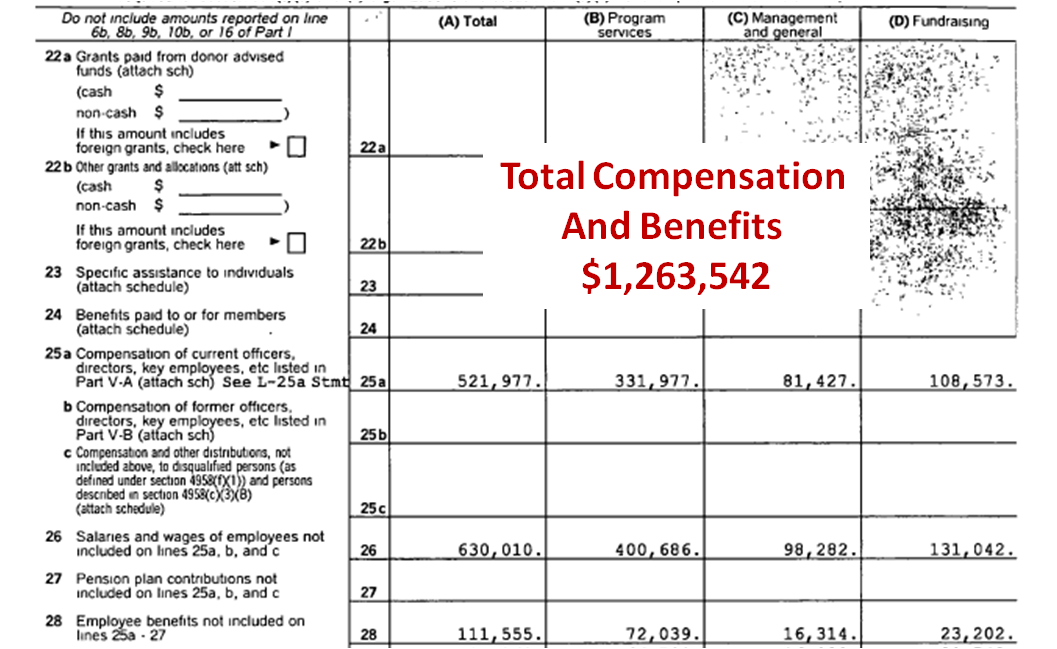

In the first two installments of this series, we covered the inconsistent reporting of revenues in the form of donations to The Second Mile (TSM) and the possible overstatement of expenses in the Foster Care and Friend/Friend Fitness Programs. We also examined the total compensation expenses that comprised nearly 60% of TSM's total expenses.

This installment examines the salary histories of Dr. Jack Raykovitz, his wife, Katherine Genovese, and the staff averages from 1998 to 2009. The chart below gives a snapshot of the histories.

Analysis - Raykovitz and Genovese

From 1998 to 2001, the increases in salaries among Dr. Raykovitz, Ms. Genovese, and the staff were all rising at similar rates between 7 and 10% each year. After 2001, the staff rate dropped precipitously, while the Raykovitz's salaries continued to on an upward trajectory.From 2001 to 2008, Dr. Raykovitz's salary increased by 33% -- rising from $99,699 in $138,279 (or a total increase of $38,630). Over that same timeframe, Katherine Genovese's salary rose 48% -- from $68,058 in 2001 to $106,013 in 2008 (or a total increase of $37,965).

The average American worker saw his/her salary increase 23% over the same timeframe (or about 3% per year).

Based on the timing of the abuse reports of Sandusky, it appears that TSM knew it had a ticking time bomb on its hands and Dr. Raykovitz took the opportunity to raise he and his wife's salary before the bomb went off.

In 2009, Sandusky was indicated as a child abuser by Clinton County Children and Youth Services and subsequently resigned from TSM (although his name and images were still used for fundraising efforts until 2011). In that year, Raykovitz and Genovese dropped their salaries by about $6K each, likely in anticipation of increased scrutiny of the charity's finances.

Despite the late drop in salaries, a number of TSM board members voiced their displeasure over what they considered exorbitant salaries for Raykovitz and Genovese. At least one board member resigned over it.

Analysis - Staff Salaries

Meanwhile, the average staff salary was fluctuating up and down from 2001 to 2007, until 2008 when TSM increased the number of total staff (less highest paid) from 19 up to 92. The IRS 990s did not provide a full listing of the staff employees, however, the increased number of staff in 2008 is an interesting development, considering that the total compensation expense increased by approximately $12K over 2007 (see below).

As was the case with revenues and expenses, it was difficult to reconcile the headcount numbers with the total compensation of the staff. Without going into great detail, there is little correlation between headcount and total compensation. In the early years, with a stable number of staff, the compensation costs are on a steady rise until 2002, then eight staff are added with hardly any increase in compensation. From 2003 to 2006, staff is relatively stable but compensation continues to escalate. And, again, in 2008 the staff jumps to 92 people and the compensation topline stays relatively flat.

Based on a source close to the charity, the staffing at the two regional offices were between 3 to 4 people, thus the staff of twelve appeared to be a good fit considering the organizational structure.

So, who was on TSM's staff and what were they doing?

It appears that the additional 73 people who were added to employment rolls in 2008 weren't being compensated very much. Or perhaps their value to the organization was simply being a number and dropping the charity's average salary to a paltry $12,215 per employee n 2009 instead of the $50,763 it was in 2007.

Conclusions

The IRS 990 forms submitted by TSM were difficult to reconcile and were often incomplete or did not include the correct forms. However, the sloppy book keeping was the least among the financial issues at TSM. From the preceding analysis, it appears that the books were being cooked at TSM and that a thorough audit (using forensic accountants) should be conducted.Next installment: Where did the money go?